ISMI

International Student Medical Insurance

A. Insurance Company: Shin Kong Life Insurance (新光人壽保險)

1.Target:

Overseas students (degree students) who do not have national health insurance coverage or overseas insurance.

2. Outpatient Clinic and Emergency Care Medical Insurance:

Description: Attending Outpatient Clinic and Emergency Care due to disease and injury.

Insurance Claim: Max. NTD1, 000.00/visit

3. Hospital Admitting Insurance:

Description: Being admitted into Hospital for treatment due to disease and injury.

Insurance Claim: Max. NTD 120,000.00/ admission

4. Daily Ward Expenses Compensation:

Description: Being admitted into Hospital for treatment due to disease and injury.

Insurance Claim: Max. NTD 1,000.00/ day

5. Important Notice:

Death and Disabilities due to accident are not included in the Insurance Claims. For more information, please refer to the Rules and Regulations of Medical Health Insurance for Mainland Chinese Students Group (新光人壽團體保險).

6. Insurance Fee:

NTD 2,910/ semester (112-1, 112-2).

7. Documents Required for Insurance Claims:

- Application Form of Insurance Claim: Please fill it out at the Overseas Students and Scholars Affairs Division of the International Office. If the applicant is the same person and wishes to claim receipts from the same hospital but with different dates, only one application form needs to be filled out.

- Original Diagnostic Report 診斷證明書正本 (sample): Please request it from the hospital or clinic. It must be stamped with the hospital or clinic seal and the physician's seal, and must include the diagnosis and the date of the medical visit. If there are multiple receipts, the Diagnostic Report must include the dates of all the receipts in order to apply.

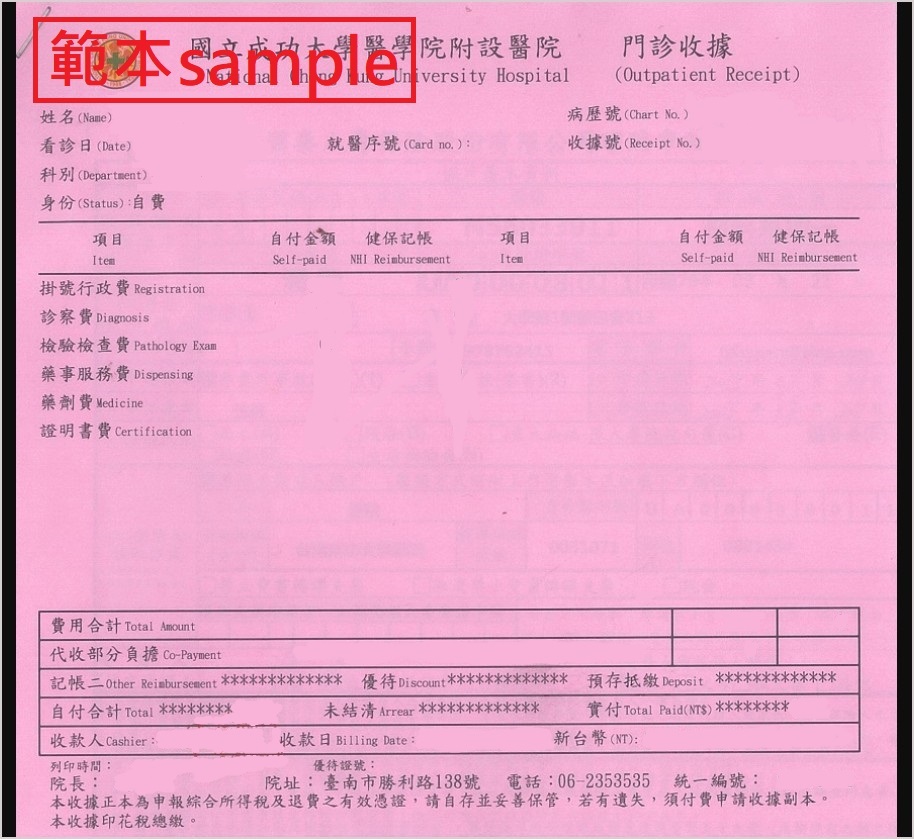

- Original of Valid Receipt(s) (sample)

- Copy of Alien Residence Certificate (ARC)

- Copy of Post Office Passbook

8. Reminder:

- Visiting Certificate 就醫證明書 is not legally equal to Diagnostic Report and it is NOT eligible for Insurance Claim.

{kind=link}

{kind=link}

{kind=link}